The Good and Bad of Credit Cards in 2025: What U.S. Customers Need to Know

Today we will know about the Good and Bad things about Credit Cards Hey there, fellow budget balancers! If you’re a U.S. customer in 2025,You will know the Good and Bad of Credit Cards in this Blog article, Suppose your chances are your wallet’s got at least one credit card nestled inside—maybe more if you’re a rewards junkie like me. They’re part of the fabric of modern life: tap them at the coffee shop, swipe them online, or pull them out when the car decides it’s time for a tantrum. But as we march through 2025, the world of credit cards is shifting—offering dazzling perks one minute and sneaky traps the next. So, what’s the real scoop on credit cards in 2025? What do U.S. customers need to know about their benefits and risks? Let’s sit down with a cozy drink, unpack the good, the bad, and the latest credit card trends, and figure out how to make these little plastic pals work for us—not against us.

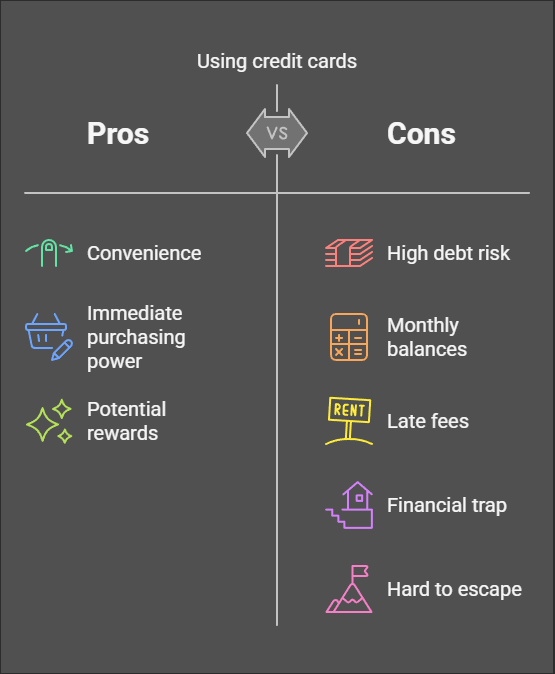

The Good: Why Credit Cards Are Still a Win in 2025

Let’s start with the sunny side—because who doesn’t love a feel-good moment? Credit cards in 2025 are like that friend who shows up with gifts and a helping hand, making life a little easier and a lot more rewarding.

-

“Ready to take control of your finances and start your journey to financial freedom? Explore our guide on The Debt-Free Journey: Overcoming Debt and Achieving Financial Freedom for practical tips and inspiration.”

Rewards That Pack a Punch

If you’re into racking up points or cash, 2025 is your year. Rewards programs are stepping up their game, and U.S. customers are reaping the benefits. Take Capital One’s Venture card—spend $4,000 in three months, and you’re looking at 75,000 miles, enough for a round-trip flight to somewhere sunny. Or Discover’s cash-back deals, hitting 5% on groceries and gas—perfect for everyday spenders. I’ve got a friend who turned her weekly Trader Joe’s run into a $50 cash-back bonus last month. It’s not just pocket change; it’s money back in your life. The benefits here are tangible—whether you’re dreaming of a vacation or just want a little extra for date night, credit cards in 2025 deliver.Credit Building Made Simple

For U.S. customers—especially millennials, Gen Z, or anyone clawing back from a financial hiccup—credit cards are still the MVP of credit scores. Issuers are rolling out beginner-friendly options like secured cards with $200 deposits or student cards with no annual fees. My sister started with a secured card two years ago—$300 limit, nothing fancy. She paid it off monthly, and now she’s got a 720 score and a card with a $5,000 limit. It’s not overnight, but it works. In 2025, apps from issuers like Chase even send you reminders or tips—like “Pay $50 now to keep your utilization low.” The benefit? A solid score opens doors to car loans, mortgages, or just bragging rights.

Convenience and Security, Upgraded

Ever tapped your phone at checkout and felt like a tech wizard? That’s credit cards in 2025 for you. Digital wallets—Apple Pay, Google Pay—are standard, and fraud protection is tighter than ever. Lose your card? Freeze it in seconds via an app. Spot a weird charge? Issuers like American Express catch it fast—sometimes before you do. I once had a $10 charge flagged from a sketchy site I’d never heard of; Amex texted me within an hour. Virtual card numbers for online buys are also a game-changer—less risk of hackers snagging your info. It’s convenience with a safety net, and U.S. customers are loving it.Your Emergency Sidekick

Life’s messy—think a leaking roof, a kid’s braces, or a pet’s vet bill. Credit cards in 2025 step up with higher limits (averaging $8,500 for good credit) and quick access. Last month, my radiator died mid-winter—$600 fix, no savings dip, thanks to my card. It’s a clutch move, but here’s the catch: it’s a loan, not a gift. We’ll dig into that next.

The Bad: Where Credit Cards Can Burn You in 2025

Now, let’s get real. For all their sparkle, credit cards in 2025 have a shadow side—and U.S. customers are feeling the heat from some serious risks.

Interest Rates That Don’t Play Nice

Buckle up: average APRs are sitting at 20.5% in 2025. Inflation’s eased a bit, but borrowing costs haven’t budged much, thanks to the Fed’s cautious moves. Carry a balance, and it’s a slow bleed. Say you spend $1,000 on a new TV and only pay the minimum—within a year, you’re shelling out $200+ in interest. My coworker learned this the hard way; he ignored a $2,000 balance for six months and owed an extra $600. The latest credit card trends show issuers banking on this—interest revenue hit record highs last quarter. It’s a profit machine for them, a wallet drain for us.Debt Piling Up Fast

Here’s a stat to chew on: U.S. credit card debt just crossed $1.13 trillion in 2025. Why? Groceries are pricier, rent’s relentless, and swiping’s too easy. About 37% of U.S. customers carry balances month to month—up from last year. Even with late fees capped at $32 (cheers to the CFPB), missing payments stacks up fast. I’ve seen friends fall into this trap—$500 here, $300 there, and suddenly they’re juggling $5,000 in debt. The risks are steep: it’s a hole that’s tough to climb out of without a plan.

Rewards That Tease

Those big bonuses and points? They’re not always a slam dunk. Some cards—like a shiny new Citi offer—promise 60,000 points, but you’ve got to spend $5,000 in 90 days. Miss it, and you’re out. Worse, redemption rules are getting trickier—points expiring in 12 months or needing double the amount for a flight. My uncle hoarded 80,000 points, only to lose half to an expiration he didn’t see coming. The latest credit card trends lean toward this bait-and-switch vibe—luring U.S. customers with glitter, then pulling the rug.Regulation Uncertainty

Here’s a curveball for 2025: deregulation talks are simmering. The new administration’s hinting at trimming the Consumer Financial Protection Bureau’s wings—think less oversight on fees or terms. If that hits, U.S. customers might face murkier statements or hidden costs. On the flip side, looser rules could mean easier credit access—great for some, risky for others. It’s a tightrope, and we’re all watching.

What’s Fresh: Latest Credit Card Trends in 2025

What’s cooking with credit cards in 2025? Let’s dive into the latest credit card trends shaking up how U.S. customers swipe and spend.

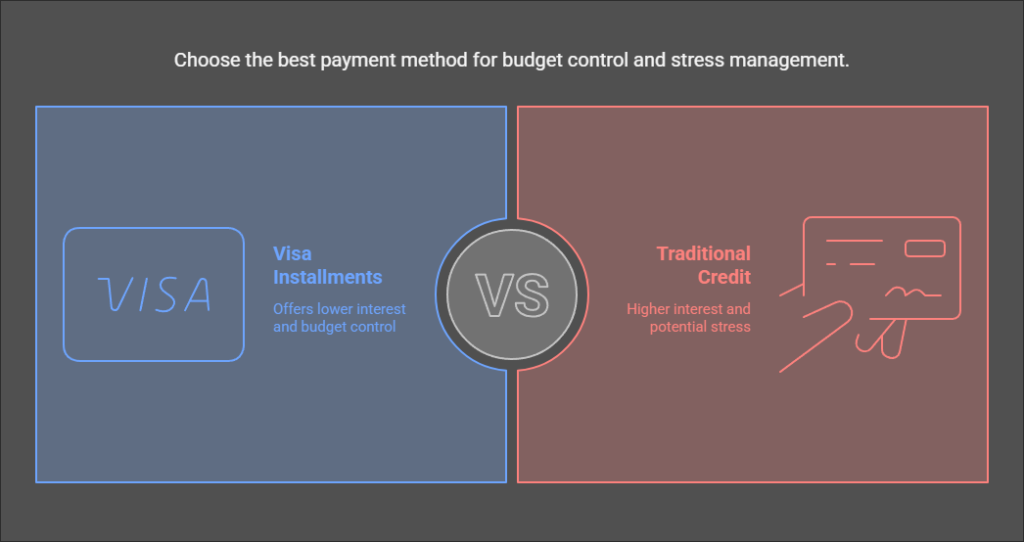

- Installments Built In

Forget standalone “buy now, pay later”—credit cards are stealing the show. Visa’s rolling out plans to split a $700 couch into four payments, often at 10% interest instead of 20%. It’s a budget hack, but miss a payment, and fees kick in. My brother used this for a laptop—loved the control, hated the stress when he almost forgot a due date.

- Gen Z’s Card Craze

Gen Z’s swiping like pros—70% have a card, chasing rewards and digital perks. They’re dropping $5 on lattes or $50 on TikTok Shop, but 35% are already in debt. It’s empowering until the bill lands—I’ve seen it with my niece, who’s learning the hard way.

- Eco Cards on the Rise

Green’s in—cards like Amex’s eco-option give bonus points for sustainable buys, like 3x at organic markets. It’s small, but U.S. customers who care about the planet are vibing with it. I snagged extra points at a local farm stand last week—felt good.

- AI-Powered Nudges

AI’s your new money buddy—flagging fraud, suggesting payments. “You’re at 75% of your limit—pay $200?” my app texted me last month. It’s smart, but it’s also more data for banks to crunch. Privacy hawks, take note.

-

“Looking for ways to grow your wealth effortlessly? Check out our guide on Passive Income and Wealth Creation Investment Ideas to get started.”

Tips to Master Credit Cards in 2025

So, how do U.S. customers tilt credit cards in 2025 toward benefits and away from risks? Here’s your cheat sheet:

- Wipe the Slate Monthly

Pay in full—every time. No balance, no interest, just rewards. It’s the golden rule my dad drilled into me, and it’s saved me thousands.

- Pick Your Perfect Match

Love travel? Grab a miles card. Stick to groceries? Cash back’s king. Our top credit card guide breaks it down by lifestyle—check it out.

- Decode the Fine Print

Bonuses expire, points vanish—set calendar alerts. And don’t overspend for a sign-up offer; I nearly did once and regretted it.

- Lean on Tools

Issuer apps track every penny—mine warned me I was $50 from my limit last week. Use them; they’re free and brilliant.

- Know When to Stop

Credit’s a tool, not a lifestyle. If debt’s creeping, pause and peek at our debt survival tips—they’ve pulled friends out of jams.

FAQ: Your Credit Card Questions, Answered

Still curious? Here’s an FAQ tackling what U.S. customers are buzzing about with credit cards in 2025:

Q: Are rewards still worth chasing in 2025?

A: Absolutely—if you’re disciplined. Cash back’s hitting 5% on everyday stuff, and travel points can score free trips. But pay off monthly, or interest wipes out the win. Watch expiration dates too—my cousin lost 20,000 points to fine print.

Q: How do I dodge credit card debt this year?

A: Spend what you can repay—full stop. Set a personal limit (say, 30% of your card’s max) and stick to it. Budget apps help, or try our debt hacks if you’re slipping.

Q: What’s up with installment plans on cards?

A: It’s a hot latest credit card trend—split big buys into chunks with lower interest. Think $800 phone over four months. It’s great for planning, but late payments pile on fees fast.

Q: Are cards safe for online shopping in 2025?

A: Yep—virtual numbers and fraud alerts have your back. My card flagged a $7 oddity last month before I blinked. Stick to legit sites, though—don’t tempt fate.

Q: Should I stress about deregulation?

A: Not yet, but stay sharp. If the CFPB weakens, fees might get sneakier. Scan statements and check CFPB news for updates.

Q: Best card for newbies in 2025?

A: Secured cards—like Discover’s—or no-fee starters are gold. Low stakes, credit-building power. Our beginner card roundup has faves.

Q: How do I pick between cash back and travel rewards?

A: Depends on you. Cash back’s instant—great for daily life. Travel points need planning but pay off big for wanderers. I mix both—cash for now, points for later.

Q: Can credit cards help in emergencies?

A: Yes, they’re a lifeline—$8,500 average limits give breathing room. But treat it like a loan, not a freebie, or you’re in debt quick.

“Discover more tips and strategies to boost your financial goals by visiting The Psychology of Financial Motivation: How to Stay Driven in a Volatile Economy in 2025.”

One Response